Significantly more is now being done to deliver operational efficiency and trade finance product innovation across both Islamic and conventional banking. CAROLINE MAGINN looks at the momentum within the sector

KSA corporate banking and trade finance continue to garner momentum because the sector has been prudently capitalised. It delivers crucial liquidity to provide meaningful supply finance to the emerging corporate segment, and trade finance is once again demonstrable as the anchor for the corporate contribution to the real economy

Banks now can do significantly more to deliver operational efficiency and trade finance product innovation across both Islamic and conventional banking. They can harmonise and integrate further their delivery of short-term and project trade finance in the interests of large corporates and SMEs. And they can also do much to bolster transparency and awareness of available trade finance tools internally and externally among customers.

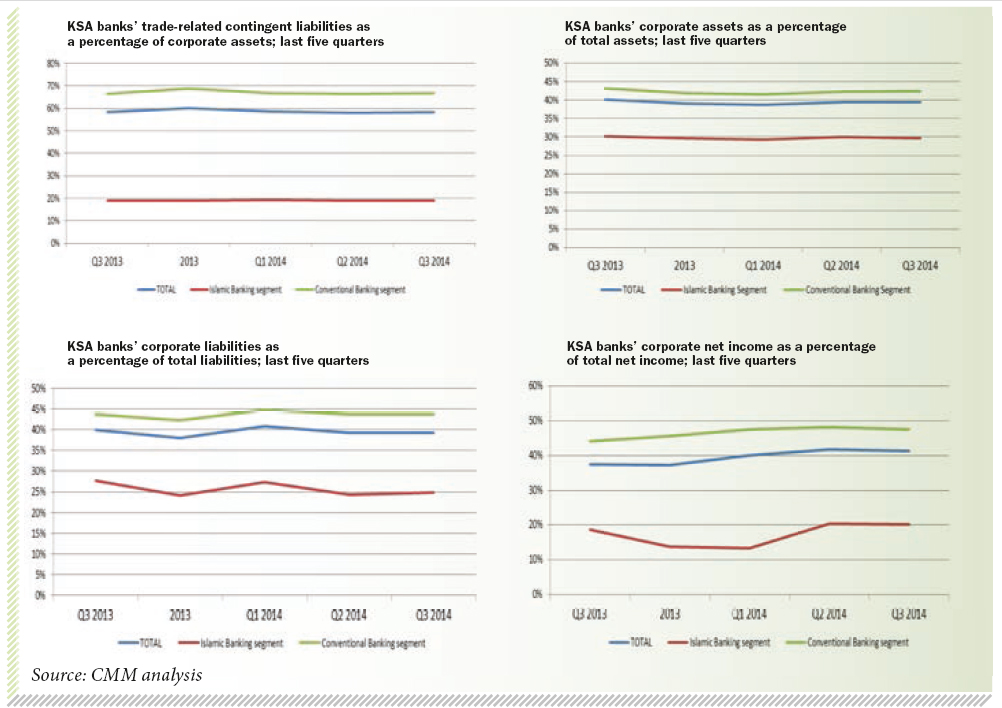

Specifically, in Q3 2014 the corporate banking and trade finance segment in the KSA continued its strong performance against the key measures, with total trade-related contingent liabilities setting a record level of more than SAR 470bn.

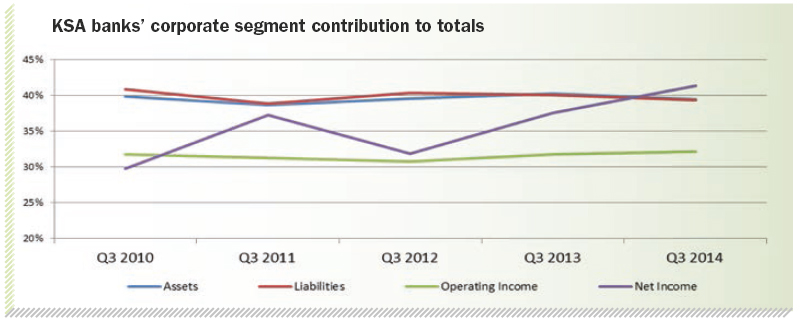

In terms of contribution to totals, corporate banking has continued to be a cornerstone contributing well over 30 per cent to total assets, liabilities, operating income and net income, and suggesting a very positive contribution from KSA banks to their corporate clients.

Trade finance, measured by the trade-related contingent liabilities at the heart of corporates’ needs, increased by 2.4 per cent from the second quarter, 2014, to, yet again, set new record figures as mentioned above.

As suggested in the previous quarterly reports, this is expected to translate into robust earnings for full-year 2014 and continues the trajectory for the eighth consecutive year.

Therefore, this would appear to be the ideal time for banks to continue to invest to improve their trade finance offerings and there should be no complacency after such a long period of sustained growth.

The mix between letters of guarantee (LGs) and letters of credit (LCs) has recently shifted further in favour of guarantees, with reported LCs edging downward for the second consecutive quarter.

This might suggest an improvement in the quality of relationships between corporates in the KSA and with their overseas counterparts and further evidence of export growth in the private sector as illustrated by the progress of corporates in promoting KSA corporate brands. Needless to say, it will be interesting to see if the trend continues over the coming quarters.

Riyad Bank continues to lead the overall CMM Corporate Banking and Trade Finance League Table and increased its rating, improving its scores in the Relative Importance of Corporate Banking and Trade Finance and of its Commitment and Capacity to Grow.

Riyad Bank also made huge strides in its provision of LGs. Conversely, those gains were somewhat counterbalanced by decreases to its LC book.

SABB increased its grip on second place in the overall table, ahead of NCB, Banque Saudi Fransi and an improving Samba. Further down the table, Al Rajhi Bank performed strongly across the series of measures.

Riyad Bank (95 per cent) also took over at the top of the table concerning trade-related contingent liabilities as a percentage of corporate assets, replacing long-time leader SABB (92 per cent). Notable positive changes in this ratio were seen in the mid-table by SAMBA (to 53 per cent) and also by Al Rajhi Bank (to 19 per cent).

The bank whose corporate assets relative to total assets ratio is highest remains Banque Saudi Fransi (58 per cent), ahead of Saudi Hollandi Bank (56 per cent) and Alinma Bank (53 per cent) with all bar three banks having a corporate contribution of more than 40 per cent.

In terms of corporate liabilities as a percentage of total liabilities, there are two banks showing at more than 50 per cent: Riyad bank (55 per cent) and SABB (51 per cent, up 4.5 per cent from Q2) and a total of eight of the 12 banks reported more than 40 per cent.

Corporate operating income as a percentage of total operating income is highest at Saudi Hollandi Bank, which reports a 56 per cent contribution. Four further banks report above 40 per cent in this category and have done consistently over the years.

The story-board for corporate net income is more remarkable with three banks reporting upwards of 60 per cent contributions to totals for the corporate segment: Saudi Hollandi Bank (63 per cent), Riyad Bank (61 per cent) and Alinma Bank (60 per cent). Banque Saudi Fransi, Bank AlBilad, SABB, Arab National Bank and national Commercial Bank report more than 40 per cent with Samba improving to just behind this group on 39 per cent.

Corporate segment assets breached SAR 800bn in Q3 2014 for the first time showing an 11 per cent increase of SAR 90bn on Q3 2013. All 12 banks reported higher figures for the quarter than the previous year with notable improvements across the table. National Commercial Bank led the way again with SAR 121bn, and lower down there was relative outperformance of the overall market by Saudi Investment Bank (+35 per cent) and Bank AlBilad (+39 per cent).

The robustness of the segment reflects a strong trust relationship between corporates and KSA banks, which could drive the provision of liquidity to support bank and corporate prosperity in the Kingdom.

Corporate segment liabilities also reached new heights in Q3 2014 with a resurgence to SAR 696bn after a slight fall in Q2. Again National Commercial Bank (SAR 167bn) leads the table with a huge 24 per cent market share (although conversely slightly below its own Q2 peak) following a 30 per cent increase on the year.

Nine of the 12 banks increased their corporate liabilities from last year with strong performances in this regard shown throughout the table. This shows the rising quality of the corporate and private sector contribution to the economy and diversification away from the level of historic dependency on oil.

Operating income for the corporate segment rose by 11 per cent on the year to more than SAR 18bn. Four banks now show net income to Q3 2014 at more than SAR 2bn with Banque Saudi Fransi joining national Commercial Bank, Riyad Bank and SABB in that achievement and Samba just below at SAR 1.9bn. All 12 banks show an increase from the equivalent quarter last year with half the banks showing double-digit percentage growth.

Corporate segment net income was up 20 per cent on the year to more than SAR 13bn with all bar one of the KSA banks reporting growth of more than 10 per cent. National Commercial Bank benefited from a rebalancing of its books from previous prudent credit provisions and took a 22 per cent market share with just short of SAR 3bn. Riyad Bank also showed above SAR 2bn and a further three banks reported figures well in excess of SAR 1bn for the period with Arab National Bank on the verge of joining this group.

Total trade-related contingent liabilities were up again on the quarter – this time by nearly 2.5 per cent on Q2 2014. Leading the way again were Riyad Bank, which reported a 25 per cent year-on-year increase for Q3.

Only one bank showed a lower total compared to the equivalent Q3 2013 and that was SABB with a marginal 0.68 per cent easing from its peak. Four banks show better than 20 per cent increases in their portfolios on the year (Riyad Bank and Samba (+21 per cent)), Saudi Investment Bank (+21.5 per cent) and Alinma Bank (+20 per cent), and a further three were above the market in terms of growth: Saudi Hollandi Bank (+15 per cent), Bank AlJazira (+13 per cent) and Bank AlBilad (+16 per cent).