20th May, 2013

- 2013 Invesco Middle East Asset Management Study

- 20% of Sovereign Wealth Fund new assets allocated to private equity

- Property and infrastructure are not the big SWF ‘alternative investment’ story

Major sovereign governments and sovereign wealth funds (SWFs) in the Middle East are increasingly considering new private equity models for investment, according to the fourth annual Invesco Middle East Asset Management Study1. Invesco opened its Dubai office in 2005, and has been working with GCC clients for decades, offering financial institutions and investment professionals access to global investment expertise.

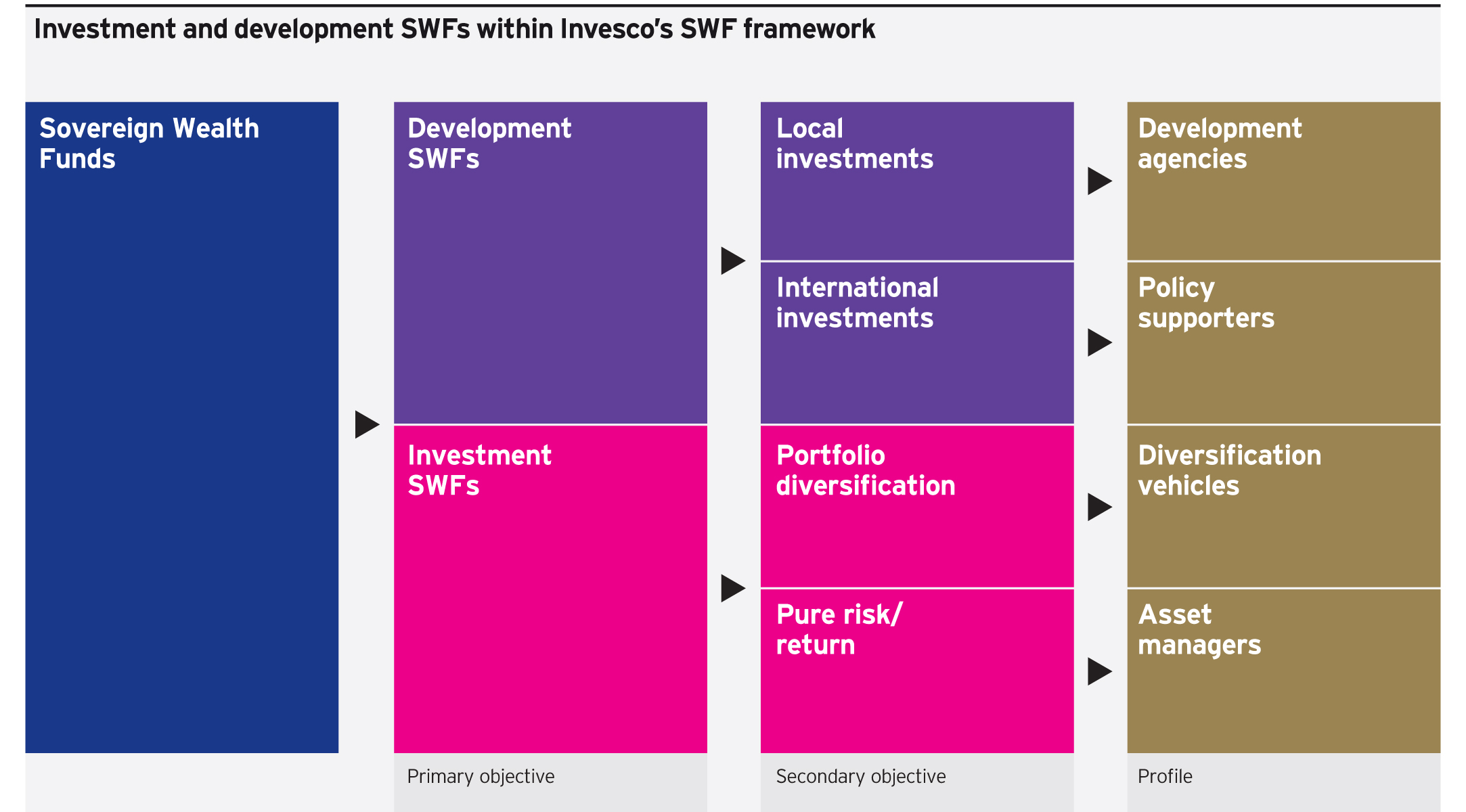

Invesco’s study, a leading in depth report, has again analysed sovereign revenues and defined the investment behaviours of major SWFs in the Gulf Cooperation Council region (GCC) which account for 35% of global SWF flows, representing $1.8 trillion2. This year it investigated the differences in risk appetite, investment preferences and asset allocations between ‘investment’ SWFs – those which aim to simply preserve and grow a country’s assets – and ‘development’ SWFs – those with the objective of generating local employment, developing skills and contributing to the GDP [see Figure 1].

In 2013, the analysis has found that private equity is the key theme to which SWFs in the Middle East are allocating. In contrast, property and infrastructure, viewed by many as the alternative investments ’of choice’ by the region’s SWFs, are viewed as less important.

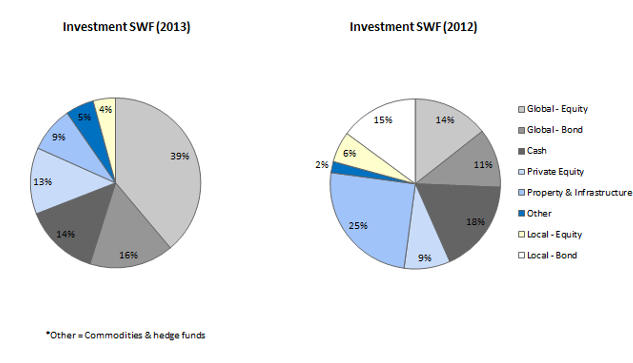

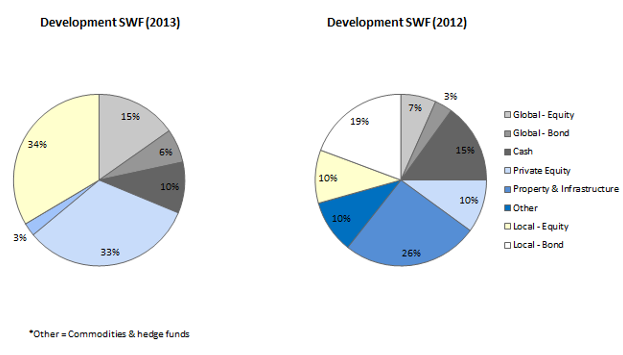

Among ‘development’ SWFs a third (33%) of new assets were on average3 allocated to private equity in the last 12 months, a huge jump compared to 10% in 2012. The study suggests that the majority of investment is via direct operations. While ‘investment’ SWFs have on average allocated 13% of new assets, driven by diversification needs as well as higher return objectives, with co-investment models being the preference. This is an increase from 9% in 2012.

Differentiating ‘development’ and ‘investment’ SWFs

The study found that as the oil price recovers, ‘development’ SWFs in the region are targeting a higher overall return for their investments with an average of 14% and allocating more assets locally, for the reasons outlined above. These development SWFs are seeing the benefit that private equity models can bring to bear as it gives them greater scope to actively participate as a shareholder in investments.

In contrast to ‘development’ SWFs, ‘investment’ SWFs on average target a return of 8% and are future generation funds that seek growth via a diversified portfolio. This explains the lower weighting to private equity and broader spread of investments across various asset classes, for example, the largest allocations within these SWFs are to global equity (39%), followed by global bonds (16%) [see Figure 2]. Diversification is the key driver behind investing in private equity. The study found the increase in allocation to private equity this year reflects a greater need to diversify away from public equities and achieve higher returns.

A commonality shared between both SWF types is the limited importance placed on property and infrastructure relative to private equity. Just 3% is allocated to infrastructure and property by ‘development’ SWFs, and 9% by ‘investment’ SWFs. This is a significant decrease from 2012 [see Figure 2].

Nick Tolchard, head of Invesco Middle East commented: “We now have a much more developed understanding of these two major and very different types of SWFs in the Middle East region. Contrary to popular perceptions these vast state funds are not piling into global property and global infrastructure projects. While we might hear about one off investments, it’s the local development objectives and vital ongoing future proofing of state reserves that take centre stage.”

Middle East SWFs moving towards direct Private-equity models

Middle East SWFs moving towards direct Private-equity models

The study identified three distinct, high-level models that SWFs were using to access private equity: 1) investment into private equity funds 2) co-investment alongside private equity funds and 3) direct investment as a standalone private equity operation. Nearly all SWFs started out investing into funds but many have moved or are considering a move to co-investment or direct models.

The study found ‘investment’ SWFs preferred co-investment because pure return objectives are aligned to other private equity investors, while ‘development’ SWFs preferred direct operations to deliver on their development objectives which are rarely shared by co-investors.

Nick Tolchard, head of Invesco Middle East concluded: “What’s really fascinating is that SWFs are looking at the private equity model as a way of investing locally; in essence becoming an active participator in the growth of local economies and putting money directly into growing enterprises to increase local jobs and build up the skill base of their people. As well as a rise in co-investment deals, over and above private equity funds, we are seeing an emergence of direct private equity investment coming out of SWFs. Clearly many feel they can compete with private equity firms directly or want to access particular strategies not aligned to the large private equity houses. It will be interesting to see how the private equity community responds to this shift.”