Quite apart from the growing risks evident in the global economy, the regional turmoil known as the “Arab Spring” resulted in sharp stock market corrections and an extreme dearth of new issuance activity in the equity, bond, and sukuk markets alike, NCB said in its report GCC Financial Market Quarterly: Back to Square One.

Quite apart from the growing risks evident in the global economy, the regional turmoil known as the “Arab Spring” resulted in sharp stock market corrections and an extreme dearth of new issuance activity in the equity, bond, and sukuk markets alike, NCB said in its report GCC Financial Market Quarterly: Back to Square One.

Having rebounded relatively quickly towards the end of Q1, stock indexes returned to pre-crisis levels and volumes rose even more, back to figures last seen in the first half of 2010. But, after that revival, the second quarter of the year has offered a much more mixed and uneven picture.

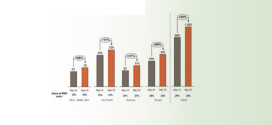

However, a clear positive momentum in bank lending is now underway in Oman, Saudi Arabia, and Qatar. Saudi Arabia, though, is the only regional economy to be witnessing a positive trend in private credit, which rose to 7.8 per cent in June. Overall bank credit in the Kingdom expanded by 7.2 per cent Y/Y, highlighting the diminishing role of public sector credit, which earlier during the crisis was the main area of dynamism.

While Qatar is still seeing fast growth in bank credit, the pace has declined steadily in recent months to reach 10.1 per cent Y/Y in May. Omani credit growth was by a whisker the highest in the region – 10.2 per cent – in May. However, the positive momentum is above all linked to public sector credit with loans to the private sector advancing by a more modest 6.1 per cent.

By contrast, credit in the UAE is still very measured – at 1.9 per cent Y/Y in April – as banks face ongoing regulatory pressures. Kuwaiti credit growth was even slower at 1.1 per cent Y/Y in June, while Bahraini bank lending actually contracted by 1.2 per cent Y/Y in May.

All is not well with the GCC economies as shown by trends in the area of bank lending, says the report.

The mixed prospects are partly due to a renewed loss of momentum in the regional stock markets during Q2. All the GCC markets lost ground during the first half of the year with the declines ranging from 0.6 per cent in Abu Dhabi and 0.7 per cent in Saudi Arabia to 10.7 per cent in Kuwait and 12.4 per cent in Oman. Any positive trends in volumes were reversed by June, as a result of which the GCC markets lost a total of $33.4bn of their aggregate capitalisation during the first half of the year.